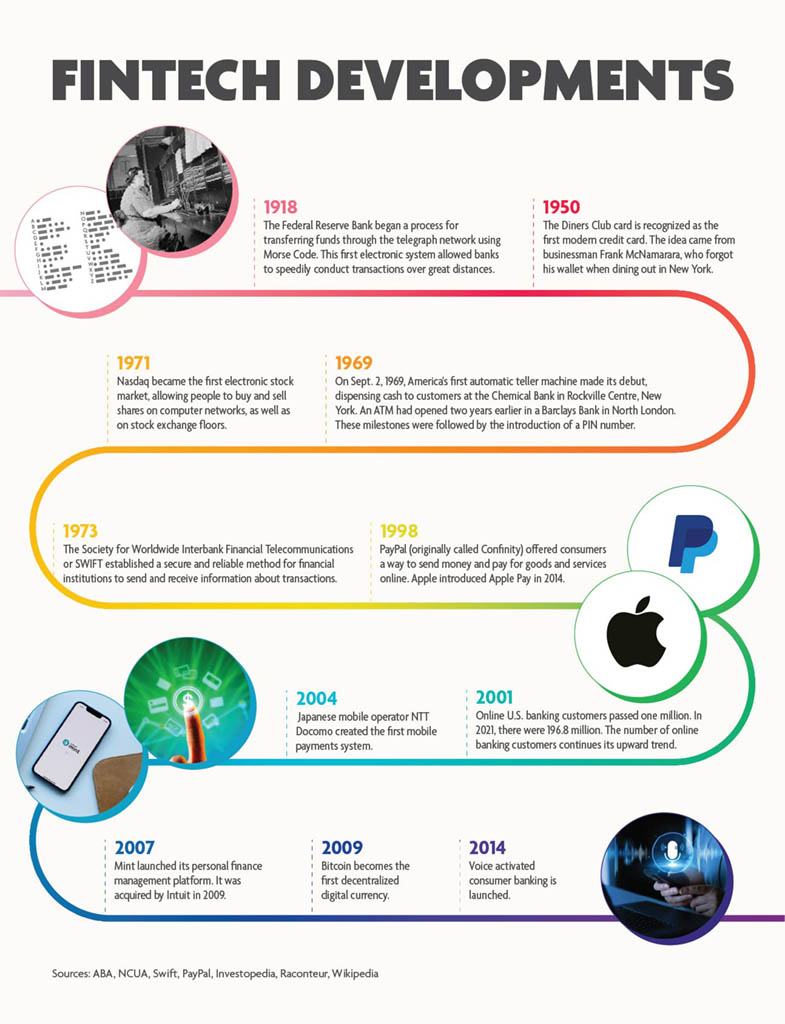

facebook

facebook

Whatsapp

Whatsapp

By Oyaol Ngirairikl, Pauly Suba and Skyler Obispo

Financial technology has revolutionized how people save, spend, and manage money. Today, mobile apps allow you to make online purchases and payments to credit cards and loans, transfer money quickly, purchase stocks and invest in your retirement.

And more recently, the power of artificial intelligence can assist individuals and financial institutions with just about everything — from rating potential investments and fraud detection to automated customer service. A November 2024 American Bankers Association survey found that more than half of U.S. consumers now prefer to bank via mobile apps more than any other method.

But on Guam and across the Western Pacific, many customers still value the human touch — stepping into a branch, speaking with a banker, or leaning on trusted institutions during life’s milestones.

Financial leaders in the region share how each institution is embracing financial technology while staying grounded in community, culture, and customer service.

What percentage of your clients currently use online banking?

Lesley-Anne Leon Guerrero, senior vice president and chief experience officer, Bank of Guam: 52% of our consumer clients actively use online banking to manage their finances and 61% of business clients leverage our digital platforms to streamline operations and enhance cash flow visibility. These figures reflect a growing confidence in digital channels, even in markets where in-person banking remains culturally significant. Our strategy is to meet customers where they are — whether that’s online, on mobile, or across our branch network.

Michael Sakazaki, senior vice president and West Pacific market president, Bank of Hawaii: Over the past few years, we’ve seen consistent growth in online banking usage, with more than 60% of our customers currently using mobile banking today.

Aurora Pimentel, senior vice president of systems operations, BankPacific: Our latest reports are tracking 51%.

Gerard A. Cruz, president and CEO, Community First Guam Federal Credit Union: Approximately 44% of our members, and growing, are signed up to on-line banking.

Gener F. Deliquina, CEO, Coast 360 Federal Credit Union: 49% of our membership are enrolled in online banking.

Jason B. Miyashita, managing director, senior vice president of investments, senior institutional consultant, international wealth advisor and private wealth advisor of Asia Pacific Group of Raymond James, Raymond James & Associates Inc.: While we don’t disclose exact usage stats publicly, we’ve seen robust growth in online and mobile engagement over the years. Our firm emphasizes strong digital engagement through our Raymond James Client Access Platform, with ongoing investments in technology to enhance efficiency and connectivity, reflecting a focus on meeting the growing demand for digital wealth management. Extending beyond our online website, Raymond James offers a dedicated Client Access mobile app, optimized for secure, on-demand access to access, including mobile check deposits and goal tracking, which has proven to be quite useful and convenient for our clients.

Sandra H. McKeever, president and financial advisor of Asia Pacific Financial Management Group: Approximately 65% to 70% of our clients utilize our online banking tools and platforms. This reflects a strong adoption of digital services among our client base.

.jpg)

Photo by Pauly Suba

How many of your clients use mobile banking apps?

Leon Guerrero: In July 2025 alone, 45,292 customers accessed their accounts via our mobile app. This underscores the increasing demand for intuitive, on-the-go financial tools. We view mobile banking not just as a convenience, but as a critical touchpoint for delivering real-time value and personalized service.

Sakazaki: While we don’t disclose specific customer counts, our mobile usage has steadily increased year-over-year and now represents the most frequently used banking method among our digital users.

Cruz: Of our on-line users, 65% use our mobile app to transact business with us. Most use our mobile banking platform for simple transactions like checking balances, making loan payments and transferring funds. Other services like wire transfers or loan closings, are done the traditional way.

Deliquina: Of the 22,000 plus enrolled in our online banking, 41% use our mobile app.

Pimentel: 32%. We want it to be more, so we’re targeting our audience to do more on online and with our app. Because it’s easy.

McKeever: About 65-70% of our clients access their accounts through our mobile apps, highlighting the importance of mobile accessibility and convenience to our clients.

Are AI Bots or automated services currently in use, and how are customers responding?

Leon Guerrero: Our AI-powered virtual banker, Cara, now handles approximately 60% of all incoming calls — a clear signal that customers are embracing intelligent automation. Cara is designed to resolve routine inquiries efficiently, freeing up our Familia Contact Center agents to focus on more complex, relationship-driven support. This hybrid model ensures we maintain both operational efficiency and the human connection our customers value.

Sakazaki: BOH has always been committed to bringing in the best technologies to make our banking services as convenient and personalized as possible. We are excited about the opportunities AI offers to serve our customers better, such as personalized financial insights and conversational interfaces in our mobile app, and our actively working to integrate AI that is trusted and secure.

Rocco Flores: We don’t have a bot yet. It may be part of our future upgrades.

Pimentel: Many of our customers appreciate that we still answer the phone personally; we don’t have an automated voice system.

John McKinnon: AI chatbots are limited to pre-programmed answers. For complex issues, our customers want to talk to someone who understands them.

Cruz: We are exploring the use of AI in our organization. This is a developing technology and we are in the early stages of adoption. AI integration for us will begin with internal infrastructure and processes, to improve operational efficiency. Using AI for loan decisioning is still a few years away. We still like being able to understand and employ human judgement into a credit decision.

Deliquina: While AI-powered banking offers many benefits, we have not introduced bots to our services. We’d like to conduct thorough evaluation of operational, legal, security, compliance, and experiential risks prior to any automation adoption. In the meantime, we explore and implement various automation of back-office processes to maximize operational resources and efficiency. AI adoption is one that we look to as a hybrid of self-service options with real human interaction to meet our members’ expectations across different generations.

Miyashita: At Raymond James, we’re harnessing the power of AI to sharpen our advisor superpowers, not to replace them. Our proprietary generative AI search platform helps improve advisor service delivery and data-driven insights for optimal client advice. The firm approaches AI prudently, focusing on leveraging AI behind the scenes to elevate the personalized services our clients value. This means that our clients get advice that’s not only personalized, but also backed by cutting-edge intelligence, whether they’re planning for retirement or navigating a complex investment strategy. In our eyes, AI is about amplifying excellence, not automating relationships, and that’s a balance our clients seem to cherish.

McKeever: While we have introduced some AI-powered tools, the majority of our clientele still prefer personalized, human interactions. Our clients often have complex financial needs that require tailored solutions and expert advice, which cannot always be addressed through automation.

What measures are in place to protect customer accounts from security breaches?

Leon Guerrero: We take a proactive, layered approach to cybersecurity. Our infrastructure includes Real-time fraud monitoring, Biometric and multi-factor authentication, End-to-End encryption, and continuous threat modeling and penetration testing. We also invest in customer education through our digital channels, because security is a shared responsibility. Our goal is to ensure that trust — our most valuable currency—is never compromised.

McKinnon: We use AI-based software that looks for anomalies and known fraud patterns. Customers can also set spending limits and get alerts.

Miranda: We use multi-factor authentication, encryption, and constant threat monitoring. We also train staff and customers to recognize scams and phishing attempts. During the major cyber event last July, we stayed fully online.

McKinnon: We send scam alerts via social media, hand out pamphlets, and test our staff internally with simulated phishing emails. Education is key for our team and for our customers.

Cruz: Cyber-security breaches are today’s single most discussed threat in our industry. In our industry, where open ports are a requirement, we live with seeing thousands of penetration attempts daily. The key to staying safe is to not stay still. So, we employ a multi-layered security program. But we also know that it’s no guarantee, so we test our program often and fix potential vulnerabilities.

Deliquina: Guarding against security breaches begins with comprehensive training for our team. Every new employee completes an in-depth information security course during onboarding, and ongoing training sessions are scheduled throughout the year to keep knowledge and skills current. Our team also receives regular updates on the latest developments in cybersecurity to stay informed and prepared.

Beyond training, our organization employs multiple layers of defense. These include physical security measures, firewalls, and endpoint protection systems on every device, all designed to detect and prevent unusual activity. We also engage third-party auditors to continually test and assess the security of our systems, both internally and externally. Vendor management is also a key focus. We rigorously vet every vendor before establishing a partnership and conduct annual reviews thereafter. This process includes analyzing their security practices and reviewing third-party audit reports.

Finally, we actively protect our members by providing ongoing security tips through our website, email alerts, social media page and in-person outreach. We also notify them promptly about phishing campaigns and other forms of scams via our online banking app and portal.

Miyashita: Protecting our clients’ assets and data is our sacred duty. Our firm mitigates security risks by employing multiple layers of protection against security breaches, including 24/7 technology safeguards to prevent unauthorized access, specialized intrusion prevention programs, and an extensive incident response team. For credit cards and accounts, measures include chip technology on debit cards to reduce fraud, encryption for online transactions, biometric options, and alerts for potential threats.

McKeever: Our firm invests heavily in cybersecurity to ensure the highest levels of protection for our clients. We utilize encrypted messaging systems, secure email platforms, and robust identity verification procedures. In addition, we conduct regular training sessions to help our team detect and prevent security breaches effectively.

.jpg)

Photo by Skyler Obispo

If fintech has changed the way businesses and individuals act towards money management and services, what has not changed at your organization?

Leon Guerrero: Our mission-driven culture remains constant. We are — and always will be — the People’s Bank. Technology enhances our capabilities, but our purpose is human at its core.

Sakazaki: While technology has transformed how we deliver services, our commitment to relationship banking remains unchanged. We continue to prioritize trust, personalized service, and community engagement—values that have guided us for generations.

Flores: People still want to work with someone they trust. Especially borrowers, they want someone they can talk to. Some of our regulars come in every Saturday, and we’re here for them. But most people now bank through mobile or online. What matters is giving them options.

Cruz: I believe that AI will not be able to replace the human factor of our business. I was taught long ago that your relationship with your loan officer doesn’t end at the time you close your first loan, it in fact begins there. And the bigger the loan, the stronger the relationship. When you experience a difficulty in life, you will want to speak with someone who knows you and can appreciate what you’re going through. AI can do many things well but what it cannot do is recognize you as a person with real life issues and offer a solution based on your individual situation. That’s what we offer here at Community First. We’re your financial neighbors.

Deliquina: Our commitment to being sensitive to the needs of our members has not changed. While we provide our members with the convenience of online banking and other electronic delivery services, we still have many members who prefer to bank and interact in person. Therefore, we ensure that the member centers (branches) continue to be accessible for in-person services Monday through Saturday. Maintaining consistent hours ensures that members can access financial services at convenient times, which is especially important for those with varied work schedules or limited internet access for online banking. Our branch hours have also allowed members to receive in-person assistance for complex transactions which would otherwise be more challenging in an online environment. We also have a unique group of well-trained, knowledgeable Contact Center team who provide personable services by actively listening and addressing member inquiries, resolving issues efficiently, and fostering strong member relationships by turning difficult interactions into positive experiences while building trust and understanding.

Miyashita: Fintech has certainly accelerated how clients interact with us digitally, but what hasn’t changed at the heart of our organization is our core commitment to personalized service and putting clients first, ensuring that human touch and insight drive trusted advisor-client relationships, rather than fully automating them. While we embrace digital innovation, we’re steadfast in our belief that wealth management is about relationships, not just algorithms. Our advisors are still the heart of our operation, delivering trusted guidance with the same integrity and care that’s defined us for decades.

McKeever: Despite the rapid evolution of financial technology, our commitment to personal service remains unchanged. Many of our clients have sophisticated financial needs that require customized, human-centered solutions. We continue to prioritize meaningful client relationships and individualized support.

What’s new at your organization?

Leon Guerrero: We’re proud to introduce Cara, our AI-powered virtual banker, and ChangeUp, a new giving and savings feature linked to our debit cards that is coming soon. This platform allows customers to round up purchases and direct the difference to either their savings account or a nonprofit of their choice. It’s a simple, elegant way to turn everyday transactions into meaningful impact — whether that’s building financial resilience or giving back to the community.

Sakazaki: The new Tamuning Branch is the first in the West Pacific to reflect Bank of Hawaii’s signature Branch of Tomorrow concept, which you’ll notice right away. It has a modern design that reflects our local community. Take our signature art as you enter: The special mural was custom created to honor the artistry and heritage of the Chamorro people. It draws inspiration from the rich history of ceramic pottery in the Marianas Islands and the decorative clay pots found in Guam’s Latte-era villages. Of course, our branch also includes the very best personalized banking experience, as well as a drive-thru ATM and 24/7 ATM and Business Depository.

Cruz: We employ a philosophy that promotes constant improvement, as a result, there is always something new here at Community First.

Deliquina: We’ve implemented mobile apps that allow our members to conveniently monitor, control, and access their debit and credit card transactions wherever they are. We continue to upgrade electronic systems by adding features that improve our members’ experiences and mitigate risks associated with this delivery channel. We have expanded our business members’ online banking access that includes stronger internal controls and convenient mobile app to conduct transactions such as mobile deposits, wire transfers, and ACH transactions from their offices, saving time and resources required for traditional in-person banking. While online banking continues to evolve to meet the needs of today’s fast-paced lifestyle, Coast360 is also embracing new ways to stay connected with our members. One exciting development is our recent expansion into Instagram. Our presence on Instagram makes a fresh chapter in our commitment to growing with the next generation of Coast360 members. In this growing digital world, social media is becoming an important extension of member service. It is another channel where our community can reach out, stay informed, and interact with us in real time. As we continue to enhance our digital platforms, our focus remains on making banking more accessible, convenient, and connected for our members.

Additionally, in the interest of reducing paper use and support a more sustainable future, members who enroll in online banking are now automatically signed up for e-Statements. This not only ensures faster, more secure delivery of important account information but also helps reduce cost. This savings allows us to continue enhancing our member service and investing in upgrades to help strengthen security in our digital platforms.

Philip Flores: We’re launching a new website soon and we’re also redesigning the Governor Joseph Flores Memorial Park sign, named after our founder. It honors our roots and legacy.

Rocco Flores: We launched the ‘Cleaning Up Our Roots’ initiative and are looking to expand into financial education next; possibly even in Palau, where a senator invited us to collaborate.

Miyashita: Recent developments at Raymond James in 2025 include appointing Chief Artificial Intelligence Officer Stuart Feld in February to drive innovation and AI business solutions. This has already borne fruit with the launch of our proprietary generative AI search platform in April, a smart tool that helps advisors access internal knowledge at faster speeds for even better client service. In May, we amped up our technology toolset further by integrating Zoom AI Companion, enhancing collaboration and productivity across the board.

McKeever: We are continually working behind the scenes to enhance our operations with cutting-edge technology. This includes the integration of AI-powered tools to streamline internal workflows and improve efficiency. Additionally, we leverage data analytics to support strategic planning and to identify emerging trends, helping us better serve our clients and adapt to a changing marketplace. Technology continues to play a vital role in our firm’s growth. While we value personal service, we recognize the importance of innovation and are committed to adopting solutions that improve operational efficiency, support informed decision-making, and enhance the overall client experience.